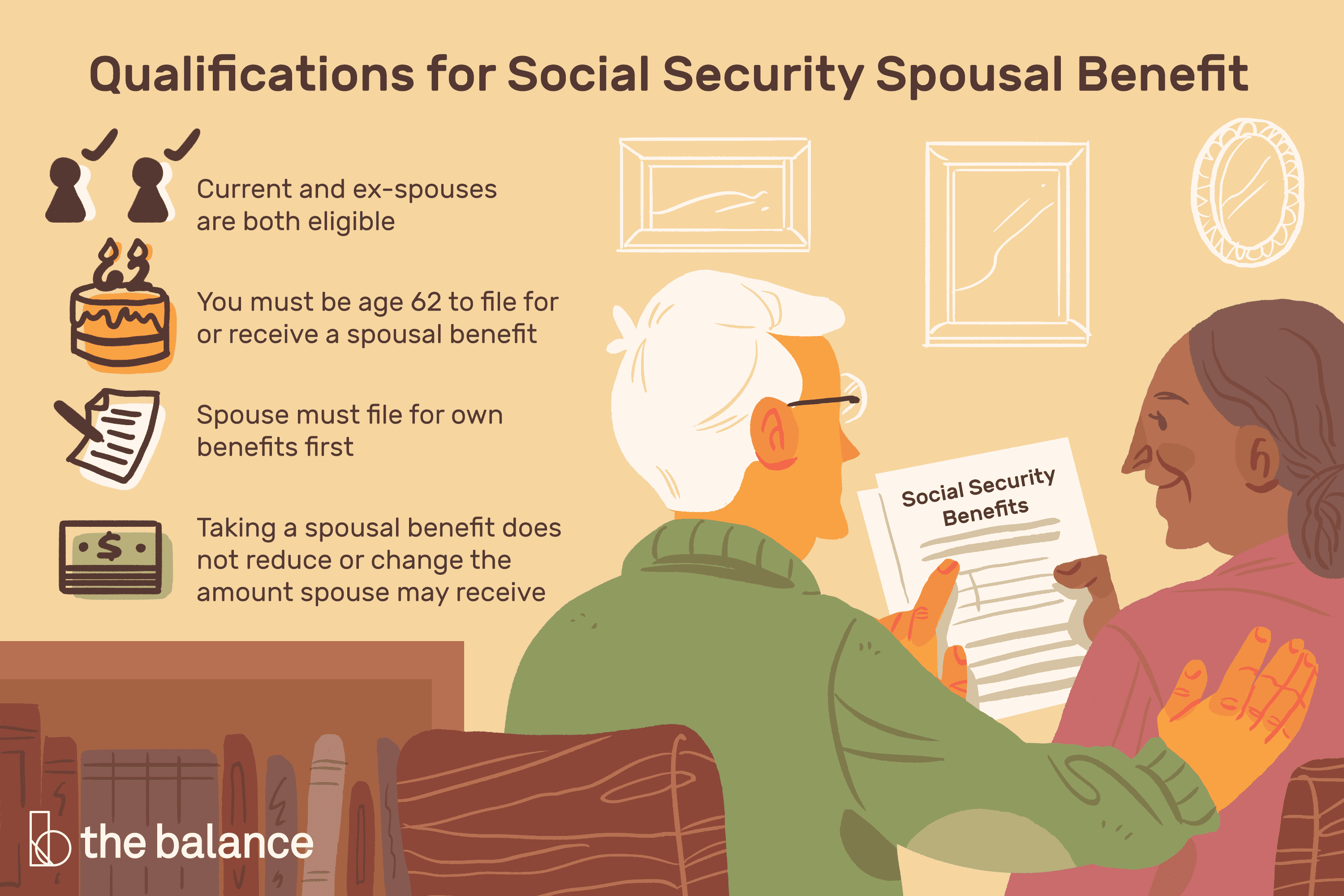

Marrying a qualified worker is the sole way to be qualified for a spousal Social Security benefit. That person is one who has put in enough time at work to accrue 40 work credits, or around ten years, or more.

However, qualifying for and receiving a spousal benefit are 2 separate things. We’ll examine more closely at why you may not receive a spousal benefit below, as well as several reasons why that would be advantageous.

How the government determines payments for spouses and Social Security

It is usually necessary to calculate the worker’s benefit before computing the spouse benefit. The first step is to calculate the median indexed monthly earnings (AIME) by adding up all of their earnings from the 35 years that they made the most money, factoring in inflation, then dividing that amount by 420.

After that, the Social Security payment formula in place in the year of their 60th birthday takes their AIME into account. A more detailed look at the 2024 formula is provided here:

- Add 90% to the first $1,174 of your AIME.

- Multiply by 32% any sum over $1,174 up to $7,078.

- Any amount over $7,078 must be multiplied by 15%.

- After combining the outcomes of the previous steps, adjust down to the closest $0.10.

The two-dollar values, referred to as the bend points, are the only components of the formula that vary yearly. If you’d like, you may view all of the bend points from prior years in a table maintained by the IRS.

The primary insurance amount (PIA), which is the outcome of this method, is not always exactly the same as the worker’s benefit. To receive this sum, the employee must file a Social Security application at full retirement age (FRA). Early enrollment can result in a 30% reduction in the worker’s pension but waiting until age 70 to enroll in Social Security can result in a 32% increase.

Benefits for spouses are determined by the employee’s PIA. The maximum payout is 50% of their PIA; but, based on when you file for benefits, you may receive as little as 35% of that amount. However, waiting until after your FRA to take Social Security benefits won’t increase spousal benefits.